Buy or sell first? Let’s bridge the gap.

Bridging Loans – what are they?

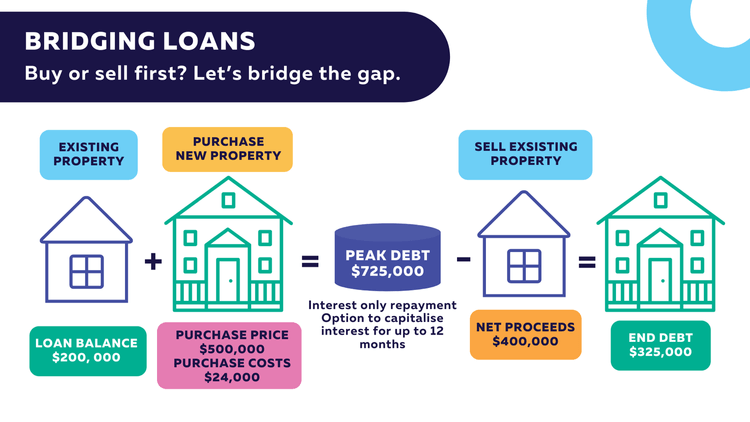

You’ve found your dream home, but you haven’t sold your existing one yet. You want to secure it before you sell your existing home so that you don’t find yourself with no-where to live. Let us help you bridge the gap.

A bridging loan is a short-term facility that covers the financial gap between the purchase of your new property and the sale of your existing property.

Eligibility

A bridging loan is available to clients who have the necessary equity in their property to be able to secure the funds required to bridge the gap between your current property and the new purchase.

A quick calculation to determine whether you may be able to secure a bridging loan is:

- The current balance of existing lending; divided by

- The estimated value of your existing property; multiplied by 100

- Will give you your current Loan to Value Ratio ( LVR – your total loan amount shown as a percentage of the value of your property).

If you current LVR is over 70%, then bridging probably is not a viable option for you, but there may be other ways to secure your property. If your LVR is below 70% you may be eligible for a bridging loan. The lower your LVR the more viable a bridging option becomes.

Benefits

A bridging loan gives you the flexibility to purchase a new property before you’ve sold your existing property. In a competitive market this could be the difference between purchasing the ideal property or missing out due to timing.

It can take the stress out of having to align your property settlement dates, to give you more control.

It allows you to borrow more money than you otherwise could under normal circumstances. This is because lenders understand that your total overall home loan debt will be reduced once you have sold your current property and paid off the bridging loan amount.

Risks

Interest is calculated daily and charged monthly, which means the longer it takes you to sell your current property, the more interest you will pay.

You may end up selling your home for less than you expected, which may leave you with a higher home loan balance than planned.

If you can’t sell your current property within the 12 month timeframe from the day your bridging loan is funded, lenders may consider this a default and step in to assist with the sale of the property.

In the event of a default, you can lose your property and you may still owe money.